Rough goal for 30's is to have 1x your annual salary in savings. So you could be doing good or bad.

Inhave that in saving, but im talking just in terms of retirement funds

Rough goal for 30's is to have 1x your annual salary in savings. So you could be doing good or bad.

Inhave that in saving, but im talking just in terms of retirement funds

Inhave that in saving, but im talking just in terms of retirement funds

*Not OK with locking those funds up or feel uncomfortable manipulating your pay, 401K, and savings account in concert with one another? Consider regular market investing in the same type of accounts you might otherwise use for retirement.

Hm, I'm 25, and I don't see myself hitting 1x my annual salary by age 30. Maybe 65-75% of my annual salary depending on how the market performs between now then. Granted, I spent a year and a half not contributing at all, and I regret that.

Hm, I'm 25, and I don't see myself hitting 1x my annual salary by age 30. Maybe 65-75% of my annual salary depending on how the market performs between now then. Granted, I spent a year and a half not contributing at all, and I regret that.

Just switch into a lower salary job sometime when you're 29.

Just switch into a lower salary job sometime when you're 29.

So are we. (If you have 1 year in an actual savings account, consider moving it.*)

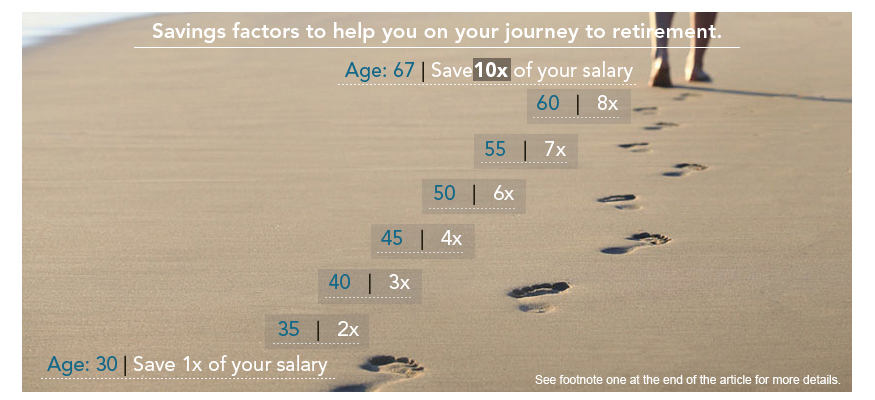

Recent guidance from Fidelity (which is just one source, so of course consult others) is someone your age should have 1 year of income in a retirement account. Apparently, this is more conservative than their guidance just a few years ago, which would have suggested a fraction of a year would have been on target.

https://www.fidelity.com/viewpoints/retirement/how-much-money-do-i-need-to-retire

That image gives you an overall idea, with more information at the link.

Something that's always bothered me about this kind of advice. I get that Fidelity and others are trying to offer a simple rule of thumb for people to check against to see if they are on track for retirement. But incomes fluctuate a lot over the course of a lifetime. Generally speaking, people will make more as they grow older (obviously not true for everyone, just a generalization here), which means both income and the ability to save goes up; it's not linear over our lifetimes. So while it's a simple rule of thumb I've actually found it to be a confusing, or at least odd, way to look at retirement savings.

I really noticed it when I got a promotion and thus a sizable raise a few years back. We put 75% of that raise to savings, nearly all of which was retirement. This really boosted the rate of our investment, but using the multiples of income as a yardstick for retirement savings, we instantly fell behind. I actually felt worse after an initial analysis using the rule income of thumb, before I realized what was happening.

The rule of thumb assumes people want to maintain their standard of living in retirement, which is probably a good assumption, but it also assumes they'll have the same expenses, which isn't. I think there are better methods, such as the 4% rule, which don't fluctuate based on income at a given point in time, but rather look at desired standard of living in retirement. They help set a target that doesn't move unless you make adjustments to it, and you can track how far along you are relative to that. Not as simple to infographic, though.

This is very much a footnote to your larger point, of course. Just thought I'd comment as it can be a discouraging way to measure progress depending where you are at.

So it's looking likely that I will be moving to the US for a few years.

I will be getting a local contract, now I know they offer a 401k, but what should I be sure to ask when we finally get down to business and start talking details?

Will I want to Roth IRA as well? Does my employer have anything to do with that?

Should I try and max out both once I arrive asap to be sure to fully utilise 2016?

Does my employer suggest companies to work with or can I ask for specific companies?

What do I want Vanguard?

I've never really paid that much attention to your US centric roth IRA/401k discussions. So now I'm looking to play catchup.

Of course if you're staying for the long term then that's a different way to look at things.

Something I am not inclined to decide at the current time.

By 'take them when you leave' what do you mean?

Let's say I leave the US and go back to Germany in 5 years. What would happen if I had a 401k and a Roth?

Really? What funds are you invested in? I have an 80/20 equities/bond split and the market has mostly recovered from the early February lows. I'm only down -1.51% now YTD.OK, I think I want to stop this bleeding and move my money out of my Vanguard SEP IRA. What are my options?

I am thinking perhaps something like a no risk investment, like a high-yield savings account. I don't expect better than 1% return...Adjusted for 3% inflation a 1% return is like -2%...Still, that's better than taking the huge losses I've been looking at for the last 6 months.

Maybe Vanguard has a savings account/money market fund? Anyone know how the taxes work with a SEP IRA?

Something that's always bothered me about this kind of advice. I get that Fidelity and others are trying to offer a simple rule of thumb for people to check against to see if they are on track for retirement. But incomes fluctuate a lot over the course of a lifetime. Generally speaking, people will make more as they grow older (obviously not true for everyone, just a generalization here), which means both income and the ability to save goes up; it's not linear over our lifetimes. So while it's a simple rule of thumb I've actually found it to be a confusing, or at least odd, way to look at retirement savings.

I really noticed it when I got a promotion and thus a sizable raise a few years back. We put 75% of that raise to savings, nearly all of which was retirement. This really boosted the rate of our investment, but using the multiples of income as a yardstick for retirement savings, we instantly fell behind. I actually felt worse after an initial analysis using the rule income of thumb, before I realized what was happening.

The rule of thumb assumes people want to maintain their standard of living in retirement, which is probably a good assumption, but it also assumes they'll have the same expenses, which isn't. I think there are better methods, such as the 4% rule, which don't fluctuate based on income at a given point in time, but rather look at desired standard of living in retirement. They help set a target that doesn't move unless you make adjustments to it, and you can track how far along you are relative to that. Not as simple to infographic, though.

This is very much a footnote to your larger point, of course. Just thought I'd comment as it can be a discouraging way to measure progress depending where you are at.

The income replacement target is based on Consumer Expenditure Survey 2011 (BLS), Statistics of Income 2011 Tax Stat, IRS 2014 tax brackets and Social Security Benefit Calculators. The 45% income replacement target (excluding Social Security and assuming no pension income) from retirement savings was found to be fairly consistent across a salary range of $50,000-$300,000, therefore this factor may have limited applicability if your income is outside that range.

...

Fidelity analyzed the household consumption data for working individuals age 50 to 65 from Consumer Expenditure Survey 2011, U.S. Bureau of Labor Statistics. The average income replacement target of 45% is based on the objective of maintaining a similar lifestyle to before retirement. This target is defined at 35% for below average lifestyle and 55% of preretirement income for above average lifestyle. Therefore, the final income multiplier target of 10x the final income goes down to 8x for below average lifestyle and increases to 12x for above average lifestyle. See footnote 4 for investment growth assumptions.

Really? What funds are you invested in? I have an 80/20 equities/bond split and the market has mostly recovered from the early February lows. I'm only down -1.51% now YTD.

If you were around in 2008 this wouldn't even count as bleeding.

Sure I'm not arguing that the second half of last year was pretty crap. But the poster said he wanted to stop this bleeding, when the market actually has been improving for almost a month now. We're definitely not bleeding anymore.I have one account that got opened around May or June of last year that is solely Vanguard Total Stock Market, and it is still down something like 5.5%. The market hasn't yet recovered from the bad luck timing points of 2015.

OK, I think I want to stop this bleeding and move my money out of my Vanguard SEP IRA. What are my options?

I am thinking perhaps something like a no risk investment, like a high-yield savings account. I don't expect better than 1% return...Adjusted for 3% inflation a 1% return is like -2%...Still, that's better than taking the huge losses I've been looking at for the last 6 months.

Maybe Vanguard has a savings account/money market fund? Anyone know how the taxes work with a SEP IRA?

If that is indeed a real income adjustment (factoring in inflation) then it does start to address the issue I had there. Good to know.I think they did address your two main points. First the model assumes a real increase in salary of 1.5% annually, so the idea of having a non-linear increase is baked in to the analysis. Of course they are not going to be able to account for someone getting a big one-time increase in salary, but then again, the milestones here are listed every 5 years, not every day. Although you may initially fall behind after getting the raise, you will eventually catch up.

This is actually why I don't like this method, or at least why it's not applicable to my situation and experience. My standard of living has changed little in the past 10 years, as my wife and I have diverted the bulk of our income increases to savings. So I can take a pay cut and still maintain the standard of living (just sans savings).As far as the argument about spending, the footnotes have this to say:

The 45% income replacement target (excluding Social Security and assuming no pension income) from retirement savings was found to be fairly consistent across a salary range of $50,000-$300,000, therefore this factor may have limited applicability if your income is outside that range.

Yes.Quick possibly dumb question, is there a way to "contribute" towards a mutual fund? Like add $100/month to it for example.

Yes.

Yes, after making the initial minimum contribution.Does Vanguard offer such mutual funds? Or can you set it to add weekly/monthly?

Thank you kindly.Yes, after making the initial minimum contribution.

https://personal.vanguard.com/us/insights/article/automatic-ira-contributions-012014

Maybe this is the better place to ask. I just found out that you get tax deductions if you do traditional Ira, and would like to recharacterize all of my Roth (from November 2014-present) into traditional, and get the tax deductions for 2015.

Anybody have any insight? Will only the amount that went into the Roth go into my traditional, or will it retroactively add the amount of money that would have been added pretax?

I want to switch to traditional regardless. So instead of having a Roth with some money and traditional going forward, isn't it better to do this and also get money back?

I'm single with 0 dependents. I figured with traditional, not only do I get a tax break, but more money is going to my IRA.

Obviously when I retire, the money will be taxed. But will it be taxed so heavily that it will negate the tax breaks I had received throughout my career? Assuming I stay at the same tax bracket, and single my whole life?

What are your thoughts on the combination Roth and traditional IRA/401k approach? It was a strategy I first learned about in a retirement seminar at work, several years ago. The idea is to have both a Roth and a traditional retirement account, and use the two together to minimize tax burden in retirement. For example by drawing on the traditional account up until the max income for the first tax bracket (10% or 15% or whatever it is in the future), and then topping off the year with Roth withdrawals, which are not taxed. That way the contributions made to the traditional accounts are getting a larger advantage and are basically guaranteed to have a lower tax burden than the contributions that went into them. It also serves as a hedge, should tax rates change unfavorably in the future.The thing to remember is that $1 in a Roth account has a higher future value than $1 in a traditional account, so even if you are contributing more to the traditional account by including the money you saved in taxes, it will have the same future value if you are assuming the traditional withdrawal is taxed at the same rate as the Roth contribution. It's worth noting that despite Roth dollars being worth more, the two account types have the same annual maximum of $5500. So if you are able to hit that maximum either way, you are actually putting more money in if you use the Roth account.

If the withdrawal was taxed at the same marginal rate, then yes, it would negate the tax break on the contribution. However, because of the way the progressive tax system works, the effective tax rate on the traditional account will usually be lower than the tax rate on the contributions if the retirement account is your primary source of income in retirement. This is because the first $X dollars get taxed at the lower rates, and only the amount you withdraw above the threshold for your current marginal tax rate will be taxed at that rate.

What are your thoughts on the combination Roth and traditional IRA/401k approach? It was a strategy I first learned about in a retirement seminar at work, several years ago. The idea is to have both a Roth and a traditional retirement account, and use the two together to minimize tax burden in retirement. For example by drawing on the traditional account up until the max income for the first tax bracket (10% or 15% or whatever it is in the future), and then topping off the year with Roth withdrawals, which are not taxed. That way the contributions made to the traditional accounts are getting a larger advantage and are basically guaranteed to have a lower tax burden than the contributions that went into them. It also serves as a hedge, should tax rates change unfavorably in the future.

But it's one of those strategies that seems to make sense on paper, but I've never actually worked out whether it plays out more advantageously. I think the lower tax burden on the traditional makes it so, but I've never sat down and run scenarios to see if that's the case.

The thing to remember is that $1 in a Roth account has a higher future value than $1 in a traditional account, so even if you are contributing more to the traditional account by including the money you saved in taxes, it will have the same future value if you are assuming the traditional withdrawal is taxed at the same rate as the Roth contribution. It's worth noting that despite Roth dollars being worth more, the two account types have the same annual maximum of $5500. So if you are able to hit that maximum either way, you are actually putting more money in if you use the Roth account.

If the withdrawal was taxed at the same marginal rate, then yes, it would negate the tax break on the contribution. However, because of the way the progressive tax system works, the effective tax rate on the traditional account will usually be lower than the tax rate on the contributions if the retirement account is your primary source of income in retirement. This is because the first $X dollars get taxed at the lower rates, and only the amount you withdraw above the threshold for your current marginal tax rate will be taxed at that rate.

I put in about 4500 last year, and will probably be going over the 5500 this year if I get a new job. I'll have to start up a traditional at that point.

You don't go over the contribution limit. The IRA, whether it is traditional or Roth, is limited by the IRS, currently set to $5500 for 2016 ($6500 if you're 50 or older) but may increase in future years (it follows inflation, but will only increase in $500 increments).

The thing you should be looking at (if you haven't already) is an employer-provided 401K plan, which allows you to contribute up to $18,000 ($24,000 if 50+) of your own funds in 2016. The typical plan is before tax (or traditional), though many plans are also now offering a Roth option (after tax). You especially want to take advantage of the 401K if your employer offers a match.

I think I have been using the wrong terms. I am in an employer Roth plan. I keep reading that if it's from the employer it's a 401k, however my paystub says that I am contributing to a Roth IRA. I also get the employer match. This is all so confusing lol. Do traditional 401k also get the same tax deduction as traditional IRA?

I think I have been using the wrong terms. I am in an employer Roth plan. I keep reading that if it's from the employer it's a 401k, however my paystub says that I am contributing to a Roth IRA. I also get the employer match. This is all so confusing lol. Do traditional 401k also get the same tax deduction as traditional IRA?

We recently switched to contributing to the traditional IRA first, because we expect our income in retirement to be significantly less than it is currently - about half. So it's advantageous for us to contribute pre-tax dollars now, avoiding a high tax bracket, and paying taxes upon withdrawal in retirement, at the lower tax bracket.The Roth has so many advantages that I definitely think it's best to utilize it first before saving in an IRA/401(k), but once you hit the Roth max, then by all means you should add to your IRA/401(k). The only disadvantage to the Roth is that you can't lower your current tax burden, that's it. In every other way, it is superior to an IRA/401(k).

We recently switched to contributing to the traditional IRA first, because we expect our income in retirement to be significantly less than it is currently - about half. So it's advantageous for us to contribute pre-tax dollars now, avoiding a high tax bracket, and paying taxes upon withdrawal in retirement, at the lower tax bracket.

What are your thoughts on the combination Roth and traditional IRA/401k approach? It was a strategy I first learned about in a retirement seminar at work, several years ago. The idea is to have both a Roth and a traditional retirement account, and use the two together to minimize tax burden in retirement. For example by drawing on the traditional account up until the max income for the first tax bracket (10% or 15% or whatever it is in the future), and then topping off the year with Roth withdrawals, which are not taxed. That way the contributions made to the traditional accounts are getting a larger advantage and are basically guaranteed to have a lower tax burden than the contributions that went into them. It also serves as a hedge, should tax rates change unfavorably in the future.

But it's one of those strategies that seems to make sense on paper, but I've never actually worked out whether it plays out more advantageously. I think the lower tax burden on the traditional makes it so, but I've never sat down and run scenarios to see if that's the case.

That is actually the strategy that I personally use. I contribute to a traditional 401K via the normal mechanism and also to a Roth account (either IRA or 401K) via the backdoor and mega backdoor loopholes. You also nailed the two reasons why I use it, although of the two I consider the hedging aspect to be more important than tax efficiency. You don't have to look that far back in American history to see tax rates that were much different than they are today, so I think it is foolish to believe that I will be able to accurately predict where my future tax rate will be relative to my current one.

If you go Roth, you have paid your dues and you don't have to worry about it. If you have an IRA, you are merely guessing what the government policy will be on Income Tax brackets when you try to take it out. Its important to remember that tax brackets can change, and really if they are going to change it will likely be up.

Yeah, that's what is known as a Roth 401(k).

https://en.wikipedia.org/wiki/Roth_401(k)#The_Roth_401.28k.29_plan

A traditional 401(k) gets the same tax deduction as a traditional IRA, and a Roth 401(k) gets the same tax treatment (taxed up front, but no taxes upon disbursement) as a Roth IRA. The only difference is that with a Roth 401(k), your employer's matching contributions are put into a separate pre-tax account and do not benefit from the same Roth tax treatment (essentially that money is in a traditional IRA).

You get two benefits with the Roth 401(k) over a regular Roth IRA. One, you're getting an employer match. And two, the limit for a regular Roth IRA is $5,500 ($6,500 if you're 50 or older), whereas the Roth 401(k) has a limit of $17,500.

Wait, the employer matching is not in a Roth account? Then that means they are matching my after tax amount, which means they are putting in less money than if I was using a traditional, no?

Wait, the employer matching is not in a Roth account? Then that means they are matching my after tax amount, which means they are putting in less money than if I was using a traditional, no?

After 401k and Roth, what is the suggested strategy for investing using post-tax money? My concern is with needing to pay taxes on distributions/dividends/etc.

I was surprised to see ~200$ in taxes for dividends/distributions and want to minimize this. I know it's post-tax and unsheltered, and I know I'm just paying taxes on new income- but I'm sure there are good strategies for this like avoiding securities with dividends/etc so I don't end up paying thousands in taxes annually years from now.

Backdoor roths a possibility?

1. Who is eligible to open an HSA?

Anyone, individuals, employees and employers, can open an HSA but you must have a corresponding high deductible health policy. More technically, an HSA can be established for any individual that meets all of the following:

- is covered by a high deductible health plan

- is not covered by another health plan

- is not eligible to be claimed as a dependent on another persons tax return

- is not entitled to Medicare benefits

Also use ETF's in a taxable account over funds - they're more tax efficient.

https://www.fidelity.com/learning-center/investment-products/etf/etfs-tax-efficiency