You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

I hate the stock market.

- Thread starter SoulPlaya

- Start date

- Status

- Not open for further replies.

David Incorporated Esq.

Member

I always have to have a laugh with coworkers who react to daily fluctuations in the market. "I just lost $3000 from my 401k! Shit!"

It doesn't matter, it comes back, grow up.

Unfortunately, when trying to help them understand what's going on I'm usually told "Ah you don't get it, I lost the money!" No, you didn't, you....ah fuckit.

It doesn't matter, it comes back, grow up.

Unfortunately, when trying to help them understand what's going on I'm usually told "Ah you don't get it, I lost the money!" No, you didn't, you....ah fuckit.

I always have to have a laugh with coworkers who react to daily fluctuations in the market. "I just lost $3000 from my 401k! Shit!"

It doesn't matter, it comes back, grow up.

Unfortunately, when trying to help them understand what's going on I'm usually told "Ah you don't get it, I lost the money!" No, you didn't, you....ah fuckit.

If they're stressin' about 3k in their retirement account they're either fucked or too young to worry about that shit.

Various Artists

Banned

I love when people don't realize you only lose when you sell. When the stock market was crashing in 08 I was putting every cent I had into it. In my opinion it was on sale. Low and behold several years later it rebounds and I use part of the profits as a down payment on a house. Go me.I always have to have a laugh with coworkers who react to daily fluctuations in the market. "I just lost $3000 from my 401k! Shit!"

It doesn't matter, it comes back, grow up.

Unfortunately, when trying to help them understand what's going on I'm usually told "Ah you don't get it, I lost the money!" No, you didn't, you....ah fuckit.

Maybe this is a bit off topic but anyway, what is "economic growth"? How does that happen? Where does it come from? I'm under the impression that economic growth is just a combination of inflation and some people getting richer at the expense of others. Please correct me if I'm wrong.

David Incorporated Esq.

Member

If they're stressin' about 3k in their retirement account they're either fucked or too young to worry about that shit.

Or 60 years old with tons of money. Some people are just weird about money. I also know younger people that watch their 401ks like hawks that don't get that it does them zero good to do so.

I love when people don't realize you only lose when you sell. When the stock market was crashing in 08 I was putting every cent I had into it. In my opinion it was on sale. Low and behold several years later it rebounds and I use part of the profits as a down payment on a house. Go me.

Exactly. I have a bit of money set aside in a pretty conservative short-term-fund that's done about 2-3% annually. I'm just waiting for a market plunge to rush it all in. It's heartbreaking to hear about people that jumped out of the market at the bottom of the crash only to rebuy once it had recovered. Fear is not only the mind killer, it is the wallet killer as well.

Your parents should be getting more conservative as they get older and therefore subject less of their investments to "stocks" and more to other assets like fixed income. There are also annuity products that can protect from the downside (at a fee, but all insurance has a fee).Mini rant coming on. Right now, the S&P 500 is falling about 20 points. This coming after the massive sell off last week that erased all of this year's gains. Yesterday, there was a slight gain, but that always happens after massive sell offs. The pattern goes, massive sell off, slight gain by people looking to get cheap stocks, then massive sell off continues.

What's the point? It's why the market is falling. It's because the economy is getting stronger. Job numbers are improving, earnings are getting better. Investors are worried that this good news might mean that the Fed will continue to slow down the infusion of billions of dollars of essentially free money into the market, and raise interest rates.

Now, who gives a shit, right? Market goes up, market goes down. Except that, we as a society, thought it was a smart idea to tie our retirement abilities into the market. My parents are nearing retirement, and their company some years ago, decided to switch from pensions to private market plans, and now their retirement funds are tied to the market. Yes, over the long term, it'll likely pay off, but now, they have to base when they retire off of some volatile index that can cause their funds to swing by thousands in a day.

Why the fuck would we tie our retirement funds to the damn stock market? Especially, one that takes good news for main street, as bad news for wall street?

The stock market is fine.

Neffarias_Bredd

Member

I would like to enter the stock market for the first time. What is some good advice to get me started?

http://www.neogaf.com/forum/showthread.php?t=749978

The How to Invest for Retirement thread. Assuming that's what you're investing for

Fun Factor

Formerly FTWer

Did Kramer have another meltdown from the stocks dropping?

If your neighbor came over every day asking to buy your house and quoting you a price that kept changing, would you freak out when the price he quoted you dropped? Or would you realize that the house you own is still the same house as it was yesterday, and will be the same house tomorrow.

Long term investing is the exact same thing. If you invest long term in profitable companies, you will make money, and a lot of it. Long term investors should not even look at the daily fluctuations of stock valuations, the only thing that matters long term are the fundamentals, so the only question a long term investor should ask is 'does this asset still make a profit'.

This is why index funds are so useful, because on average most companies are profitable, if not they wouldn't stay in business. So for an index fund investor the only thing that should cross their mind when the price of stocks drop is that they should buy more.

Long term investing is the exact same thing. If you invest long term in profitable companies, you will make money, and a lot of it. Long term investors should not even look at the daily fluctuations of stock valuations, the only thing that matters long term are the fundamentals, so the only question a long term investor should ask is 'does this asset still make a profit'.

This is why index funds are so useful, because on average most companies are profitable, if not they wouldn't stay in business. So for an index fund investor the only thing that should cross their mind when the price of stocks drop is that they should buy more.

CyclopsRock

Member

That's true but at the same time, your money being in a given share or fund should be contingent on your expecting it to go up (or, in the case of individual shares, possibly a decent dividend yield) - what you put in, whilst personally important, actually has 0 to do with future potential earnings and if you can help it should have no bearing on where your money is put. In other words, of you lose 50% of your investment on a fund and the beat option for an investment is Fund B, you really should move it even if that means "leaving behind" your loss.Pretty much...invest in a fund and hold onto that sucker. Downturns in the market are the best times to invest, everything is on sale. The only time you actually lose money is when you sell out and lock in a loss.

If you're nearing retirement, you should not be heavily invested in stocks

Boom Boom Pow

Banned

Where would you rather us tie our retirement fund to then? bonds?

Wait for a big drop. Invest. Pull out after ~3 years. Repeat?Think long term bro... I got burned hard in 2000 and 2008.. didn't sell, it all came back... It always comes back....................................................

.

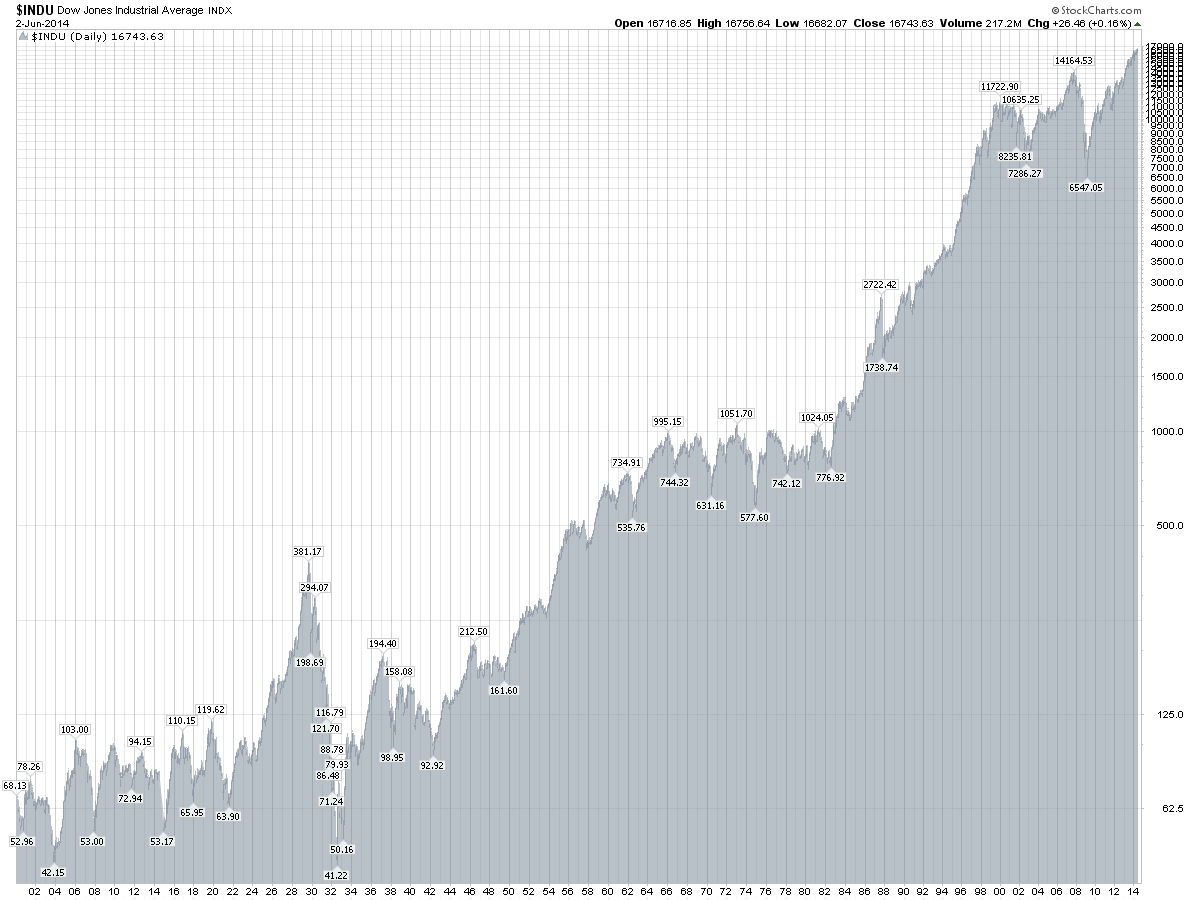

Here is a graph of the last 100 years. See a trend?

I'm gonna be a billionaire.

The stock market is pretty much divorced from real economy for quite a while now.Mini rant coming on. Right now, the S&P 500 is falling about 20 points. This coming after the massive sell off last week that erased all of this year's gains. Yesterday, there was a slight gain, but that always happens after massive sell offs. The pattern goes, massive sell off, slight gain by people looking to get cheap stocks, then massive sell off continues.

What's the point? It's why the market is falling. It's because the economy is getting stronger. Job numbers are improving, earnings are getting better. Investors are worried that this good news might mean that the Fed will continue to slow down the infusion of billions of dollars of essentially free money into the market, and raise interest rates.

Now, who gives a shit, right? Market goes up, market goes down. Except that, we as a society, thought it was a smart idea to tie our retirement abilities into the market. My parents are nearing retirement, and their company some years ago, decided to switch from pensions to private market plans, and now their retirement funds are tied to the market. Yes, over the long term, it'll likely pay off, but now, they have to base when they retire off of some volatile index that can cause their funds to swing by thousands in a day.

Why the fuck would we tie our retirement funds to the damn stock market? Especially, one that takes good news for main street, as bad news for wall street?

And you hit the nail on the head with retirement, the citizens of the US were conned by wall street, the 401k model is a terrible idea, it's just a way for the financial sector to make more money.

A special government retirement bond like they have in Canada is not a terrible idea (I'm talking in general, I'm not overly familiar with the program details) but more broadly, it doesn't make a whole lot of sense to ask people to individually save for retirement. You can't know how much you're going to need, you effectively running an insurance program for one person, that mean that the prudent thing to do is to oversave (i.e. put aside more money than you're statistically likely to need), which is great for wall street, but bad for you and bad for the economy (because you have less money to spend).Where would you rather us tie our retirement fund to then? bonds?

The stock market is pretty much divorced from real economy for quite a while now.

And you hit the nail on the head with retirement, the citizens of the US were conned by wall street, the 401k model is a terrible idea, it's just a way for the financial sector to make more money.

A special government retirement bond like they have in Canada is not a terrible idea (I'm talking in general, I'm not overly familiar with the program details) but more broadly, it doesn't make a whole lot of sense to ask people to individually save for retirement. You can't know how much you're going to need, you effectively running an insurance program for one person, that mean that the prudent thing to do is to oversave (i.e. put aside more money than you're statistically likely to need), which is great for wall street, but bad for you and bad for the economy (because you have less money to spend).

We (and most other nations) have those, they are called savings bonds, and they are shit.

As an effectively 100% secure investment, treasury bonds will always have shit yields.

Stocks outperform all other securities by an order of magnitude over basically any decently long period, so in an ideal situation a 100% stock allocation is ideal if the risk is acceptable.

There have only been like 10 years since 1940 where the 3 year annualized return was negative, like 5 years where the 5 year annualized return was negative.

There have been no years where the 10 year return was negative, and there have been no years where the 20 year return was less than 6.5 percent, much less negative.

The absolute worst 25 year period from 1952-2002 returned 7.94%, and the best 25 year period over the same time span returned 17.24%.

IMO unless you are retiring within 5 years, there is almost no reason to be invested in treasuries. Long term stocks win out over every form of bond imaginable.

Also your statement about oversaving being a bad thing (for anyone involved) is completely false, because it only looks at one part of that equation. You are looking at the money that is not spent instead of the yield earned on that investment, and how much more than money achieves over the long term. I mean it's not like people save for retirement by putting the money under their mattress. Worst case scenario it is in a savings account at a bank who is using it to lend to other people.

What is Aristus's object in saving 10,000 francs? Is it to bury them in his garden? No, certainly; he intends to increase his capital and his income; consequently, this money, instead of being employed upon his own personal gratification, is used for buying land, a house, &c., or it is placed in the hands of a merchant or a banker. Follow the progress of this money in any one of these cases, and you will be convinced, that through the medium of vendors or lenders, it is encouraging labour quite as certainly as if Aristus, following the example of his brother, had exchanged it for furniture, jewels, and horses.

For when Aristus buys lands or rents for 10,000 francs, he is determined by the consideration that he does not want to spend this money. This is why you complain of him.

But, at the same time, the man who sells the land or the rent, is determined by the consideration that he does want to spend the 10,000 francs in some way; so that the money is spent in any case, either by Aristus, or by others in his stead.

With respect to the working class, to the encouragement of labour, there is only one difference between the conduct of Aristus and that of Mondor. Mondor spends the money himself and therefore the effect is seen. Aristus, spending it partly through intermediate parties, and at a distance, the effect is not seen. But, in fact, those who know how to attribute effects to their proper causes, will perceive, that what is not seen is as certain as what is seen. This is proved by the fact, that in both cases the money circulates, and does not lie in the iron chest of the wise mall, any more than it does in that of the spendthrift. It is, therefore, false to say that economy does actual harm to trade; as described above, it is equally beneficial with luxury.

But how far superior is it, if, instead of confining our thoughts to the present moment, we let them embrace a longer period!

Ten years pass away. What is become of Mondor and his fortune, and his great popularity? Mondor is ruined. Instead of spending 60,000 francs every year in the social body, he is, perhaps, a burden to it. In any case, he is no longer the delight of shopkeepers; he is no longer the patron of the arts and of trade; he is no longer of any use to the workmen, nor are his successors, whom he has brought to want.

At the end of the same ten years, Aristus not only continues to throw his income into circulation, but he adds an increasing sum from year to year to his expenses. He enlarges the national capital, that is, the fund which supplies wages, and as it is upon the extent of this fund that the demand for hands depends, he assists in progressively increasing the remuneration of the working class; and if he dies, he leaves children whom he has taught to succeed him in this work of progress and civilization.

In a moral point of view, the superiority of frugality over luxury is indisputable. It is consoling to think that it is so in political economy, to every one who, not confining his views to the immediate effects of phenomena, knows how to extend his investigations to their final effects.

http://bastiat.org/en/twisatwins.html

Price Drop

Member

Each day is essentially random and doesn't have anything to do with a company's fundamentals. It's all about how which hedge fund with a computer or high frequency trader can buy and sell to get a quick buck. The percentage drops or gains after earnings are ridiculously baseless, it's simply a movement of thousands of shares out of a stock that didn't gain to another that may gain.

Almost all stocks are shorted so it just makes it impossible for most Americans to believe in a 'buy and hold' strategy or believe in the stock market period.

Almost all stocks are shorted so it just makes it impossible for most Americans to believe in a 'buy and hold' strategy or believe in the stock market period.

- Status

- Not open for further replies.