You're actually taking assets from the pretty well-off youth, not everyone else.

a lot of the youth get a roughly good deal. Let's review.

A. young people can stay on their parents' insurance til 26.

B. young people will qualify for a lot of subsidies

C. young people will often qualify for the medicaid expansion

D. Most young people who don't qualify for subsidies generally have employer insurance anyway, so they don't even come into the equation.

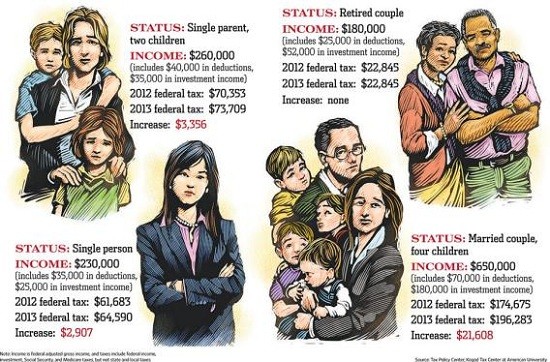

What's really happening is Obamacare is asking healthy people w/o employer insurance who make over 4 times the poverty level in addition to the youth getting cheap coverage in order to pay more to subsidize people who can't afford insurance now or can't get it at a reasonable rate because of a pre-existing condition

I'm 28 years old. A contract worker trying to pay my way back through a second degree. I make a little under 34,000 a year before taxes. I pay 900 a month in rent, 550 a month in tuition, 100-200 in utilities. A car note, car insurance, food, necessities, gas and still have to buy things like textbooks and school supplies.

Read my post history about my support of obamacare and UHC. You'll find I was at one time one of this forums most vocal advocates.

Now how the fuck you continue to try and spin this current iteration of the law as anything but a complete fuck you to many of the youth today is beyond me. It's literally asking me to pay money I can't afford for the privledge of paying another 5000-6000 dollars if anything were to actually be seriously wrong with me. It's horseshit. It's subsidizing the poor and the old on the backs of the youth(which honestly would be fine if done in a responsible manner, because its how insurance works, but that isn't happening now) who can barely(if at all) afford it. And don't give me this crap that its better to pay 6000-8000 instead of 100,000. Me and most in my situation will still end up in a dire situation if it occurs. And for the majority that nothing will occur, they live with an even worse financial situation and less disposable income in a fragile economy that is in desperate need of increased consumer spending and demand.

And dont just think im some odd exception. i worked in the service industry for many years. imagine the difficulty of a moderately successful server/bartender making 30,000 a year but sporadically and inconsistantly. maybe one year they qualify for subsidies but not the next. or the trouble that will come in the summer slow season when utilities are high and income is low but the healthcare bills still roll in. The fact you and others are jumping through hoops having to explain away these criticisms should set off the self-reflective bells.

The democrats lack of balls, like with most of their major legislative initiatives for the last thirty years, is so compromised because of a pussyfied backbone that they compromise what is initially good legislation in favor of shitty legislation that leaves their opponents still angry at them and alienates many of the people they initially tried to help because they are so concerned with the appearance of bipartisanship and appearing centrist that they constantly start at an already compromised position and just move further and further to the right on everything. Scared to admit that government isn't some evil boogeyman like Reagan framed it and that in instances, like healthcare, government administrated care is the ONLY fair and logical course of reform. Maybe if they started at the lefts equivelent of the republicans ideas we might have at least ended up with something that doesn't completely fuck many of today's youth. Which just may risk burning some bridges with a demographic that they have overwhelmingly dominated in terms of support.

So now we have a law that is still vehemently hated by the people they wanted to persuade. And in the process they fucked over many of the people they wanted to support and then there are those not in either camp who are only seeing marginal benefits which isn't going to be enough to build a coalition to push further reform and in turn might just have created enough apathy and/or dissent that a growing opposition will be able to neuter if not completely repeal the law in coming years.

And sadly enough I am struggling right now with who I actually want to support coming up because democrats don't have the balls to fix this clusterfuck but republicans do. But their answer means a worse situation for everyone and a regression of the national conversation that probably won't spark back up for at least another decade.

Once again democrats screwed themselves by screwing the very people they aimed to help.

")